Title: Streamline Your Wealth Management Operations with Multi-Portfolio Managing Software: A Comprehensive Solution for Back Office Integrations and Sales Integrations

Introduction:

In today's fast-paced financial landscape, managing multiple portfolios efficiently is crucial for wealth management firms and investment companies. The need for a comprehensive software solution that integrates various back-office functions and sales integrations has become increasingly important. Custom Portfolio™ offers a powerful wealth management software that combines several essential tools, including Forecast Screener, Fixed Income Finder, Cross-Reference Position Report, Performance Reporting, Duration Reporting, Daily Cash, and Tax Loss Harvesting. This article will explore the benefits of using such software and how it can save money through low-cost budget optimization when setting up a hedge fund or investment company.

1. The Power of Multi-Portfolio Management Software:

Multi-portfolio management software, like Custom Portfolio™, provides a centralized platform that allows wealth managers to efficiently handle multiple portfolios simultaneously. This eliminates the need for manual tracking and reduces the risk of errors. With a single software solution, wealth managers can seamlessly integrate various back-office functions, including portfolio analysis, risk management, compliance monitoring, and reporting.

2. Back Office Integrations:

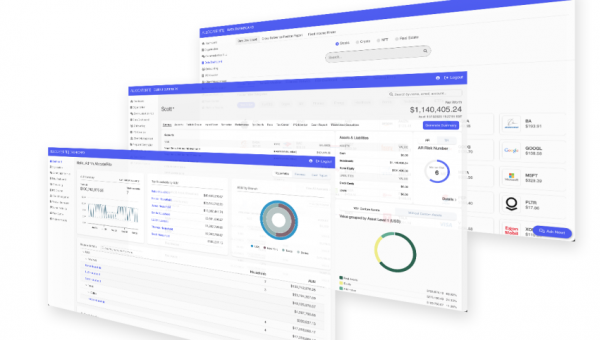

Custom Portfolio™ offers a range of back-office integrations, enabling seamless connectivity between different systems and processes. By integrating forecasting tools, such as the Forecast Screener, wealth managers can make informed investment decisions based on accurate and up-to-date market data. Fixed Income Finder allows for efficient identification and analysis of fixed income securities, streamlining the investment process. Cross-Reference Position Report ensures accurate tracking of positions across multiple portfolios, reducing the risk of discrepancies and improving operational efficiency.

3. Sales Integrations:

The sales integrations provided by Custom Portfolio™ enable wealth managers to effectively manage client relationships and drive business growth. Performance Reporting allows for comprehensive reporting on portfolio performance, enabling wealth managers to showcase their expertise and attract new clients. Duration Reporting provides insights into the duration risk of fixed income portfolios, helping wealth managers align investment strategies with client objectives. Daily Cash integration ensures efficient cash management across portfolios, reducing idle cash and maximizing returns. Tax Loss Harvesting tools help optimize tax efficiency by identifying opportunities to offset capital gains with capital losses.

4. Low-Cost Budget Optimization:

Setting up a hedge fund or investment company can be a costly endeavor. Custom Portfolio™ offers a cost-effective solution by combining multiple functionalities into a single software platform. By eliminating the need for separate systems and reducing manual processes, wealth managers can achieve significant cost savings. Moreover, the software's scalability allows for easy expansion as the business grows, avoiding the need for expensive system upgrades or additional software licenses.

Conclusion:

In conclusion, Custom Portfolio™ offers a comprehensive wealth management software solution that integrates multiple portfolio management tools, back-office functions, and sales integrations. By streamlining operations and eliminating manual processes, wealth managers can enhance efficiency, reduce errors, and save costs. The software's low-cost budget optimization makes it an ideal choice for setting up a hedge fund or investment company. Embracing the power of technology through multi-portfolio managing software is a smart investment in today's competitive wealth management industry.

Please contact us if you want to setup back office, front office and trading desk with high sophisticated integrated software email: This email address is being protected from spambots. You need JavaScript enabled to view it.